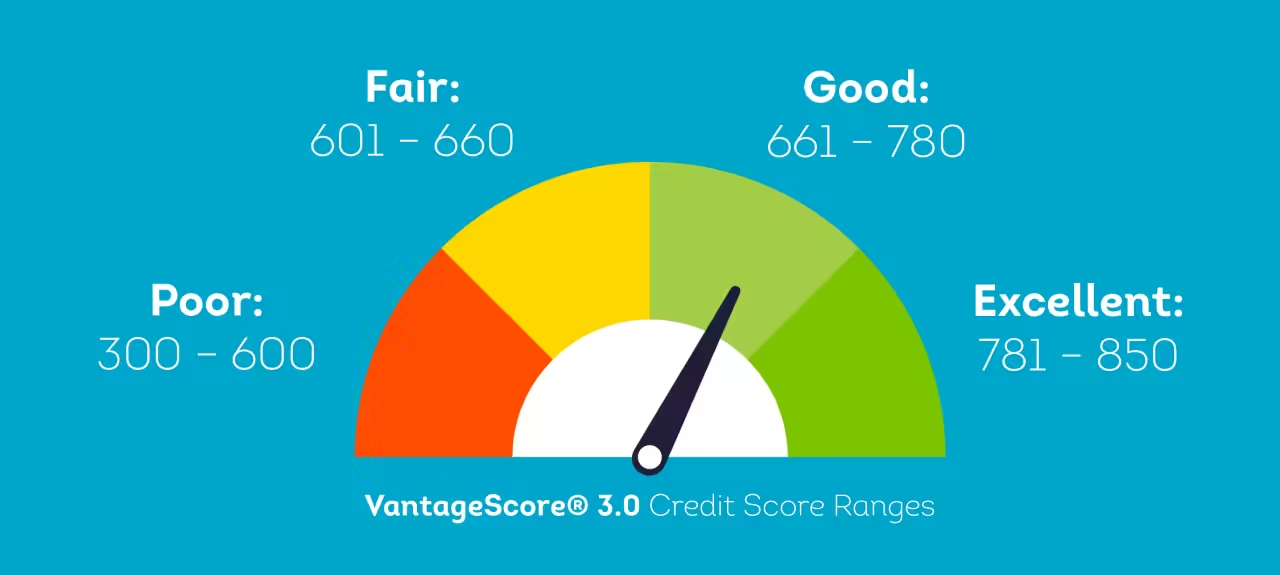

VantageScore vs. FICO 2026

Your Credit Karma score and your mortgage lender’s score can differ by 50 points or more — and both are technically correct. They’re measuring the same credit history through two different mathematical models. Understanding which model applies to your situation is the most useful piece of credit literacy most people never learn.

Short answer: for any loan application that matters — mortgage, auto, personal loan — your lender is almost certainly using a FICO score. For day-to-day monitoring, VantageScore works fine. Here’s why, and what to do with that information.

Table of Contents

What each model is and who created it

FICO (Fair Isaac Corporation) invented credit scoring as we know it. The company released its first credit score in 1989. Today, over 90% of top US lenders — including virtually all mortgage lenders, major auto lenders, and most credit card issuers — use one version of the FICO score in their underwriting process, according to FICO’s own lender data.

VantageScore was created jointly in 2006 by the three major credit bureaus — Equifax, Experian, and TransUnion — as a competing model. VantageScore 3.0, launched in 2013, is the version most apps and free monitoring services use today. VantageScore 4.0, the more recent version, is gaining traction: Fannie Mae and Freddie Mac were directed by FHFA guidance in 2023 to transition to using VantageScore 4.0 alongside FICO 10T for mortgage underwriting — a transition that is underway but not yet complete as of April 2026.

How they calculate your score

Both models use the same 300–850 scale and the same underlying input data — your credit report. The difference is how they weight the factors.

| Factor | FICO 8 Weight | VantageScore 3.0 Weight |

|---|---|---|

| Payment history | ~35% | ~40% |

| Amounts owed / utilization | ~30% | ~20% |

| Length of credit history | ~15% | ~21% |

| New credit / inquiries | ~10% | ~5% |

| Credit mix | ~10% | ~13% |

The weightings are approximate — both companies treat the exact percentages as proprietary. The differences explain why the same person can have a different score under each model.

The paid collections difference — one of the most impactful practical distinctions:

- FICO 8: A collection account that has been paid off still negatively affects your score.

- VantageScore 3.0: Paid collections are ignored entirely; only unpaid collections count against you.

This means people who have paid off collections often see their VantageScore significantly higher than their FICO Score 8. If you are monitoring your score with a free app and see a high number, then apply for a mortgage and get a lower number, this is a likely culprit.

Thin file handling:

- VantageScore can generate a score with as little as one month of credit history and one account.

- FICO Score 8 requires at least one account open for six months and at least one account reported to the bureau within the past six months.

First-time credit users with minimal history may have a VantageScore but no FICO Score 8 yet.

Which FICO version is actually being used?

FICO itself is not one score. Multiple versions exist, each optimized for different lending decisions.

| FICO Version | Primary Use | Update Year | Availability |

|---|---|---|---|

| FICO Score 2 | Mortgage (Equifax data) | 1998 | myFICO paid plans |

| FICO Score 4 | Mortgage (TransUnion data) | 1998 | myFICO paid plans |

| FICO Score 5 | Mortgage (Experian data) | 1998 | myFICO paid plans |

| FICO Score 8 | Most credit cards and personal loans | 2009 | Experian free app, myFICO, many credit cards |

| FICO Score 9 | Some auto and personal lenders | 2014 | myFICO paid plans |

| FICO Score 10 | Emerging use | 2020 | Limited availability |

| FICO Auto Score | Auto lending | Multiple versions | myFICO paid plans |

| FICO Bankcard Score | Credit cards | Multiple versions | myFICO paid plans |

The mortgage industry gap: US mortgage lenders are currently required by Fannie Mae and Freddie Mac to use older FICO versions — FICO Score 2 from Equifax, FICO Score 4 from TransUnion, and FICO Score 5 from Experian. These are versions from 1998. A transition to FICO Score 10T and VantageScore 4.0 is underway through the FHFA, but as of April 2026, the classic mortgage FICO scores are still the primary models used at closing.

This means: the FICO Score 8 you access free through Experian’s app is still not the score your mortgage lender will use. The mortgage-specific FICO scores are only available through myFICO paid plans at the Advanced ($29.95/month) or Premier ($39.95/month) tier.

Why your scores differ across apps

Five sources of score variation, in order of impact:

1. Different scoring models. Credit Karma uses VantageScore 3.0. Experian’s free app uses FICO Score 8. myFICO provides FICO 8, plus older mortgage FICO versions. All are correct for what they claim.

2. Different bureaus. Credit Karma uses Equifax and TransUnion. Experian uses — naturally — Experian. Capital One CreditWise uses TransUnion and Experian. Not all lenders report to all bureaus. A late payment reported to Experian but not to TransUnion creates a real difference between your Experian and TransUnion scores.

3. Different snapshot dates. Your credit file changes when lenders report new information, typically monthly. A score from Credit Karma updated on the 5th and a score from Experian updated on the 15th reflect different snapshots of the same underlying account.

4. Calculation timing. A large credit card charge that posts before a statement closing date briefly spikes your utilization. If two apps pull your data on different days relative to statement cycles, they may calculate materially different utilization percentages.

5. Data discrepancies between bureaus. Some lenders report to only one or two bureaus. An account that exists on your Equifax file may not exist on your TransUnion file, producing genuinely different credit profiles at each bureau.

What to do with this information

For everyday monitoring: Use any free app consistently. The exact number matters less than the trend — is your score going up or down? Both FICO and VantageScore track the same underlying factors; the trend will be the same across models.

Before a credit card or personal loan application: Check your FICO Score 8. It’s available free through Experian’s free app, Discover (cardholders), American Express, and several other card issuers. This is the score most credit card and personal loan underwriters will use.

Before a mortgage application (3–6 months in advance): Check your mortgage FICO scores. These are FICO Score 2 (Equifax), FICO Score 4 (TransUnion), and FICO Score 5 (Experian). They’re only available through myFICO’s Advanced or Premier paid plans. A 10-point difference between your FICO Score 8 and your FICO Score 5 can change your mortgage rate tier.

Before an auto loan: Check your FICO Auto Score. Available through myFICO paid plans. Auto lenders use a specific scoring model that weighs your history with auto loans more heavily than the base FICO Score 8.

To improve your score in any model: Payment history is the single most impactful factor in both FICO and VantageScore — roughly 35–40% of your score. Paying every account on time, every month, is the most reliable path to improvement in any model. Reducing your credit utilization (balance divided by credit limit) below 30% is the fastest single action with measurable short-term impact. The CFPB’s guide to improving your credit score explains each factor in plain language.

VantageScore 4.0 and the future of credit scoring

VantageScore 4.0 includes trended data — it looks at the direction of your balance over time (are you paying down or building debt?) rather than just the snapshot. A consumer paying down a balance scores higher under VantageScore 4.0 than under VantageScore 3.0, even if the balance is still substantial.

The FHFA’s 2023 directive to transition Fannie Mae and Freddie Mac to using VantageScore 4.0 alongside FICO 10T is the most significant shift in US mortgage underwriting in decades. When the transition completes, it will mark the first time a VantageScore is used in conforming mortgage decisions.

Frequently asked questions

Is FICO or VantageScore more accurate?

Neither is more accurate — they’re different. Both calculate scores from the same credit report data using different weightings and algorithms. FICO Score 8 is the standard for most US lending decisions. VantageScore 3.0 is the standard for most free monitoring apps. “More accurate” depends on which purpose you’re asking about.

Can I improve one score without improving the other?

The fastest way to create a gap is to pay off collection accounts. Paying a collection improves your VantageScore 3.0 immediately (paid collections are ignored). Your FICO Score 8 will still reflect the collection record — though its negative impact diminishes over time. For all other actions — paying on time, reducing utilization — improvements flow to both models proportionally.

Why does my Credit Karma score change but my Experian score doesn’t?

Credit Karma updates your TransUnion and Equifax VantageScores weekly. Experian’s free app updates your FICO Score 8 monthly. A change visible on Credit Karma in the last 7 days may not yet appear in Experian’s calculation because the Experian update hasn’t pulled the new data yet.

Do employers see FICO scores?

No. When an employer runs a credit check (permitted in some jurisdictions for certain positions), they see a modified credit report — not any credit score. The report shows account history, balances, and payment patterns, but no numeric score.